If you are approved for Federal Disability Retirement you will get an annuity that is calculated based off your High 3 average salary.

What is the High 3 Average for Federal Disability Retirement?

Your high-3 average pay is the highest average basic pay you earned during any 36 consecutive months of service. Your basic pay is the basic salary you earn for your position and it does not include payments for overtime, bonuses, etc.

The High 3 Average is calculated by the OPM and is often your most recent 36 months of pay, however, this is not always the case, and many factors can affect the final number.

Working while on Federal Disability Retirement

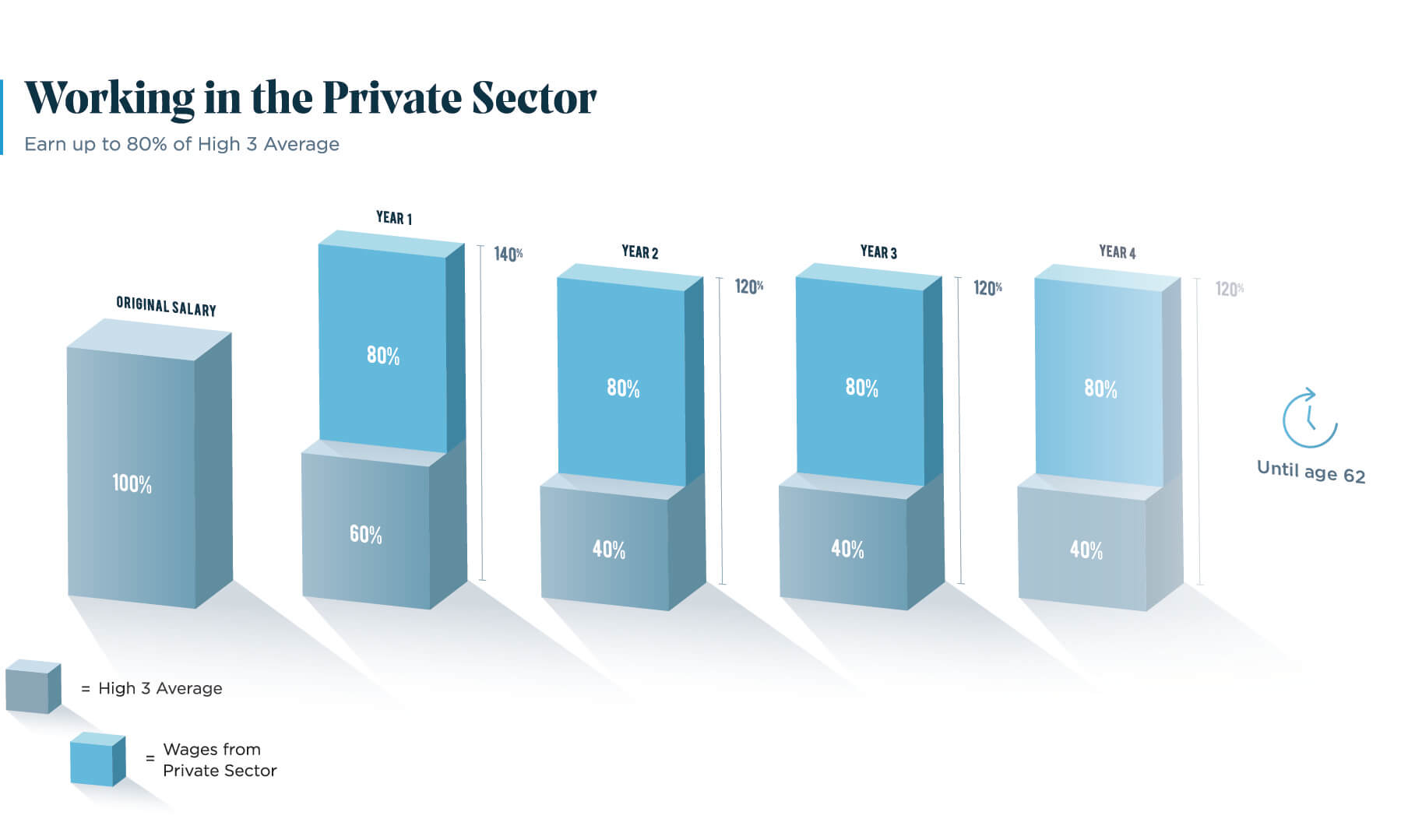

Unlike other benefits (i.e., OWCP Workers’ Compensation), once approved for the Federal Disability Retirement annuity, you can continue working in the private sector and earn up to 80% of your original position’s salary. The income from your private sector job would be in addition to your Federal Disability Retirement annuity (if it remains under the 80% range).

The graph below illustrates the income potential while receiving the disability retirement annuity and working in the private sector.

The Federal Disability Retirement Annuity continues until you reach the age of 62 at which time it will recalculate into regular retirement. It is also important to note that the 80% income cap only applies until the age of 60. From 60-62 you can earn additional income without any limits.

Why is this so important?

This opportunity will give you the chance to potentially earn more in your disability retirement than you would have made while working in your position for the federal government.

For example, if your High 3 is $100,000 then you would receive $60,000 for the first 12 months on Federal Disability Retirement and then $40,000 every year thereafter until 62. If you choose to work in the private sector, then you can earn up to $80,000 a year. This would allow you a total potential income of $140,000 for year 1 and $120,000 for year 2+. This can be a huge benefit as it would allow you to earn more than your current income and have a base income that is secure through age 62.

But what if you can’t work while on Federal Disability Retirement?

While this annuity can provide a safety net to explore the next stage of life, many federal employees are unable to continue working, even in the private sector, due to their disability. This annuity gives them the freedom to retire and still receive a consistent and secure income stream until their regular retirement kicks in.

Annual Income Survey

It’s important to know that each year disability annuitants under the age of 60 must submit an income survey to the OPM. They will analyze your responses and determine if you will continue to receive disability retirement annuity payments or if your earned income was greater than the 80% earning limit. If your 80% earning limit is exceeded, then you will be considered restored to earning capacity and will no longer receive federal disability annuity payments.

Remember, if you are over the age of 60 you will no longer have an 80% earning limit. Your earned income will no longer be restricted, and you will still receive your disability annuity payments until you are the age 62.

Keep in mind that your private sector job must be within the restrictions that were listed under your Federal Disability Retirement. For example, if your medical restrictions for Federal Disability Retirement state that you are not able to stand for more than 4 hours, then your new private sector job should fall within those restrictions as well.

Even though you can seek employment after approval, it is recommended that you do not return to work in the federal government as that might negatively impact your Federal Disability Retirement eligibility.

Important note- The OPM also conducts annual medical reviews to ensure you are still eligible for disability retirement annuity payments.

Here is a list of possible job opportunities in the private sector based on feedback from previous Federal Disability Retirement clients.

- Teacher

- Child Care Provider

- Real Estate Agent

- Dental Assistant

- Paralegal

- Bank Teller

- Private Security Officer

- Customer Service Specialist

- Office Assistant

- Insurance Agent

- Writing Assistant

Earned income vs. Passive Income

When looking for a job within your 80% income cap range, take into consideration your earned income and passive income.

Earned income on Federal Disability Retirement

This type of income would apply to your 80% earning limit.

Earned, or active, income includes money earned from a job such as salaries, wages, bonuses, and tips. It also includes self-employment income, such as from work done as an independent contractor, and income from a business that you actively participate in. This category also includes alimony that you receive, as well as certain forms of retirement income like pensions and distributions from 401(k)s and traditional IRAs. While these forms of income are not being actively earned, they are taxed as such.

Passive income on Federal Disability Retirement

This type of income would NOT apply to your 80% earning limit.

Passive income includes income from real estate investments; including investments in actual properties, as well as dividend income received from REITs. It also includes income from limited partnerships (businesses in which you are invested but don’t play an active role) and certain other types of tax-sheltered investments. This passive income is not included in your 80% private sector income cap which gives you the opportunity to earn more than you were making at your federal job.

Don’t forget about Creditable Years of Service

One of the most important aspects of the Federal Disability Retirement benefit is the ability to continue to receive creditable years of service towards your regular retirement. So, even if you are not working for the federal government, you will continue to receive creditable years of service for each year you are on the benefit just as if you were still employed with the federal government.

For example, if you worked 15 years as a federal employee and received federal disability retirement benefits for 20 years, then you would have a total of 35 creditable years of service towards your regular retirement.

This can play a significant role when your final regular retirement calculation is made at 62 and can increase your regular retirement annuity for the remainder of your life.

The Federal Disability Retirement benefit is a nuanced and confusing topic. It is critical to understand the long-term impacts on you and your family. We recommend scheduling a free consultation with our office to look at the benefit in context of your situation and find the best path forward for you.

If you are a federal employee that is needing to apply for Federal Disability Retirement or if you have any questions on your specific case, then contact us today to set up a FREE consultation.